Maximizing Your Retirement Savings: Strategies You Need to Know

Unlock essential strategies to boost your retirement savings and secure a financially stable future

RETIREMENT STRATEGIES

Matt CFA, CFP®

5/16/20245 min read

Retirement savings can feel like a daunting task and the average retirement savings gap in the U.S. is noteworthy, with many falling short of their retirement needs. Fidelity recommends having 10x your final salary saved by age 67. For a $100,000 final salary, that’s $1 million compared to the average 401(k) balance for those aged 60-69 is only about $195,500.

However, with the right strategies, you can maximize your nest egg and ensure financial security in your golden years. Here’s a comprehensive guide to the best ways to maximize your retirement savings if your income allows for it, including 401(k) investments, IRAs, Backdoor Roth IRA, Mega Backdoor Roth, and a Health Savings Account (HSA).

401(k) Contributions

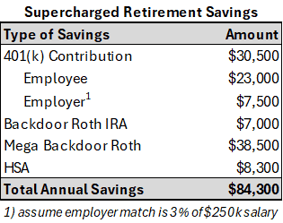

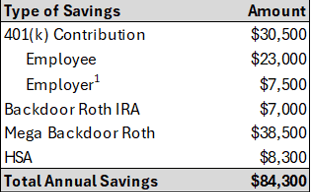

A 401(k) plan is one of the most powerful tools for retirement savings. Contributions are made with pre-tax dollars, which can lower your taxable income and allow your investments to grow tax-deferred. Take full advantage of your employer’s matching contributions. This is essentially free money that can significantly boost your retirement savings. For 2024, the maximum contribution limit for a 401(k) is $23,000, with an additional catch-up contribution of $7,500 for those aged 50 and above. By consistently contributing to your 401(k) and taking advantage of employer matching, you benefit from compounding interest. For instance, contributing an extra $5,000 annually over 25 years could add up to an additional $316,000, assuming a 7% return on investment.

Individual Retirement Accounts (IRAs)

IRAs are another cornerstone of retirement planning, offering both traditional and Roth options.

Traditional IRA: Depending on your income and whether you have a retirement plan at work, contributions to a traditional IRA can be tax-deductible. For instance, if your modified adjusted gross income (MAGI) is less than $123,000 (for married filing jointly) in 2024, you can fully deduct your IRA contributions (max contribution of $7,000 or $8,000 if above age 50), reducing your taxable income and potentially saving hundreds to thousands in taxes annually. Additionally, investments grow tax-deferred meaning you don't pay taxes on the investment earnings until you withdraw the money in retirement. This can potentially result in substantial growth over time as your investments compound without the drag of annual taxes.

Roth IRA: A Roth IRA offers numerous benefits that make it an attractive option for retirement savings. Contributions are made with after-tax dollars, allowing investments to grow tax-free, and qualified withdrawals in retirement are also tax-free, providing significant tax savings over time. Unlike traditional IRAs, Roth IRAs do not require minimum distributions at any age, allowing investments to grow for as long as you choose. Additionally, beneficiaries can inherit a Roth IRA without owing federal income taxes on withdrawals, provided the account has been open for at least five years, which is advantageous for estate planning. The tax flexibility in retirement is another benefit, as withdrawals do not count as taxable income, helping manage tax liability and potentially keeping you in a lower tax bracket. Furthermore, there is no age limit for contributing to a Roth IRA as long as you have earned income, enabling continued savings into senior years.

For the 2024 tax year, you can contribute up to $7,000 to either a Roth IRA or a traditional IRA, and if you are 50 or older, you can contribute an additional $1,000, making the total $8,000. However, this limit is the maximum amount you can contribute across both types of IRAs combined. In other words, you cannot contribute the maximum amount to both a Roth IRA and a traditional IRA within the same tax year; your total contributions to both accounts cannot exceed $7,000 (or $8,000 if you're 50 or older).

Backdoor Roth IRA

If your income exceeds the limits for contributing directly to a Roth IRA, you can use the backdoor method to still take advantage of the Roth’s tax-free growth and withdrawals. There are a few steps involved but in essence a Backdoor Roth IRA is set up just as its name implies; open a traditional IRA and then convert those funds to a Roth IRA. This strategy allows high-income earners to sidestep income limits. You will pay taxes on any pre-tax contributions and earnings at the time of conversion, so it’s best to convert the amount to a Roth IRA shortly after making the contribution. Since the contribution was non-deductible, the conversion should generate little to no taxable income if set up properly.

Mega Backdoor Roth

The Mega Backdoor Roth IRA stands out as a powerful tool. It allows high-income earners to meaningfully boost their retirement savings in a tax-advantaged way, even when they exceed the income limits for traditional Roth IRA contributions. The Mega Backdoor Roth IRA is an advanced retirement savings strategy that allows individuals to convert after-tax contributions from their 401(k) plan into a Roth IRA. This process can increase the amount one can save in a Roth account beyond the standard contribution limits. In 2024, the IRS allows employees to contribute up to $23,000 to their 401(k) if they are under 50 years old, or $30,500 if they are 50 or older. This is the pre-tax or Roth 401(k) contribution limit. However, many 401(k) plans permit after-tax contributions beyond the standard limits. In 2024, the total combined contribution limit (employer and employee) to a 401(k) is $69,000 ($76,500 if age 50 or older). Once after-tax contributions are made, they can be converted to a Roth 401(k) within the plan (if the plan allows) or rolled over into a Roth IRA. This conversion is where the "backdoor" comes in, as it circumvents the usual income limits for Roth IRA contributions.

Health Savings Account (HSA)

An HSA offers a triple tax advantage: contributions are tax-deductible, growth is tax-free, and withdrawals for qualified medical expenses are tax-free. HSAs can also be used as an additional retirement account. For 2024, you can contribute up to $4,150 for individual coverage or $8,300 for family coverage (including employee and employer contributions), with an additional $1,000 catch-up contribution for those aged 55 and older. Unlike flexible spending accounts (FSAs), HSAs do not have a “use it or lose it” rule, allowing your contributions to grow over time. Many HSAs offer investment options similar to 401(k)s and IRAs.

Final Thoughts

By leveraging these strategies—maximizing 401(k) contributions, utilizing Backdoor and Mega Backdoor Roth IRAs, and contributing to HSAs, you can significantly enhance your retirement savings. Each strategy offers unique tax advantages and growth potential, so it's crucial to understand how they fit into your overall retirement plan. According to the Employee Benefit Research Institute, people who regularly maximize their 401(k) contributions can have over $1 million more in retirement savings than those who don't. It truly pays to maximize your contributions and take advantage of employer matching.

3857 Pell PL Unit 103 San Diego, CA 92130

mk@hevelcapital.com

(636) 236-9039

All content is for information purposes only. It is not intended to provide any tax or legal advice or provide the basis for any financial decisions. Nor is it intended to be a projection of current or future performance or indication or future results.

Opinions expressed herein are solely those of Hevel Capital, LLC and our editorial staff. The information contained in this material has been derived from sources believed to be reliable but is not guaranteed as to accuracy and completeness and does not purport to be a complete analysis of the materials discussed. All information and ideas should be discussed in detail with your individual adviser prior to implementation. Advisory services are offered by Hevel Capital, LLC an Investment Advisor in the State of California. Being registered as an investment adviser does not imply a certain level of skill or training.

The information contained herein should in no way be construed or interpreted as a solicitation to sell or offer to sell advisory services to any residents of any State other than the State of California or where otherwise legally permitted.

Images and photographs are included for the sole purpose of visually enhancing the website. None of them are photographs of current or former Clients. They should not be construed as an endorsement or testimonial from any of the persons in the photograph.

Purchases are subject to suitability. This requires a review of an investor’s objective, risk tolerance, and time horizons. Investing always involves risk and possible loss of capital.