Market Update: May 2024

Growing Concerns in US Stocks

MARKET UPDATE

Matt CFA, CFP®

5/1/20245 min read

There are significant moving pieces and powers at play in global markets and I am not an economist nor have any desire to be one. However, my expertise is in investments and have been quoted in major financial publications (e.g., WSJ, CNBC, Bloomberg, etc.) dozens of times in prior roles. I’m not sharing this to brag but to bring perspective…which is that there are a lot of ‘talking heads’ out there but nobody can consistently and accurately predict the future. There are always unforeseen events (black swan events) that are by nature unpredictable (e.g., COVID). Market fluctuations and black swan events are why having a diversified portfolio across asset classes that is dynamically rebalanced to meet your tailored goals is essential. I think this is enough for a long-winded disclaimer and mini-plug…now onto the market update.

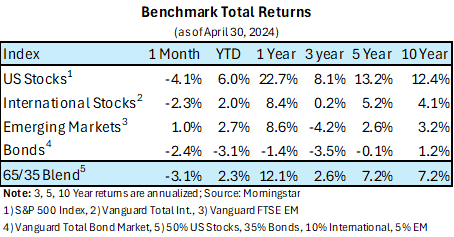

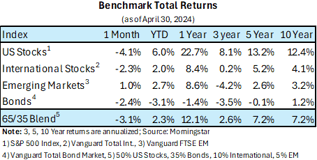

US stocks finally took a small setback in April following strong gains over the past year. Following steep declines in 2022, markets recovered (US stocks leading the way) due to expectations for an accommodating Federal Reserve as inflationary forces subside. The ‘market’ is made up of individuals who buy and sell securities based on perceived fair value. Value is assessed through expectations for future performance. Simplistically, US stocks have performed well over the past year due to market expectations for lower inflation numbers and subsequent Federal Reserve interest rate cuts. However, inflation has remained stickier than expected and therefore the Fed has paused its ‘cuts’ causing the market to slightly sell off in April.

There are growing reasons to be concerned with US stocks (long-term, US stocks tend to climb the ‘wall of worry’ so market timing has proven to be a futile task) including high valuation levels, geopolitical risks, and inflation that just won’t go away. Let’s tackle each of these in more detail.

1. High valuation levels:

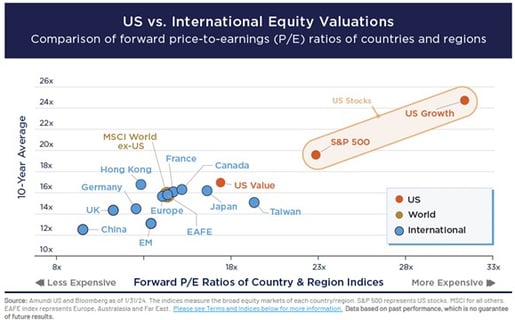

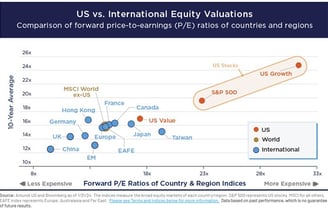

US stocks are trading at a price/earnings multiple above their historical average and at premiums to the rest of the world which has led to strong market performance. However, returns have been concentrated in Large Cap Tech over the past few years due to market exuberance around artificial intelligence. While you’ll never time the ‘top’ just right which is why ‘time in the market’ is more important than ‘timing the market’, high-flying growth stocks will likely mean revert over time…even AI companies. Therefore, it is important to diversify your portfolio to include international and emerging markets despite inferior performance over the past decade and the temptation to overweight expensive tech stocks.

2. Geopolitical Risks:

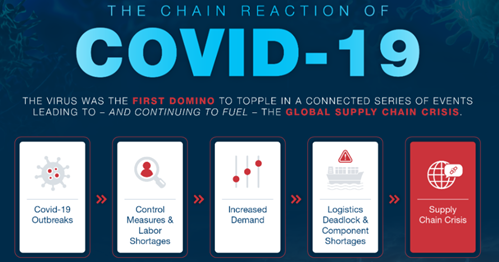

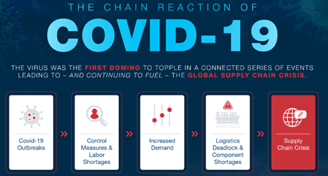

Geopolitical risks are always prevalent but as the world de-globalizes and becomes a multi-polar world, there is a higher risk of disruptions. This happened when Russia invaded Ukraine resulting in a prolonged war and thousands of lives lost. From a financial perspective, the war has disrupted the commodities market (Ukraine was one of the top exporters of grain and wheat with a global market share of 10%+ (OEC World)) and during the pandemic as the entire world shut down for various lengths of time. The pandemic shutdowns led to inventory shortages in most industries as supply chains were disrupted and the government (including the Fed) inflated demand through stimulus and rate cuts. The economy is still working through inflationary impacts from this supply-demand shock (e.g., elevated house prices due to lack of supply as homeowners are stuck in place due to low mortgage rates).

I believe that geopolitical risk is much broader than the upcoming US election and increasing polarization on the home front. In fact, there is a record-breaking 77 global elections this year (JP Morgan). Conventional wisdom states that geopolitical risks generate more noise than impact but this year may challenge that notion.

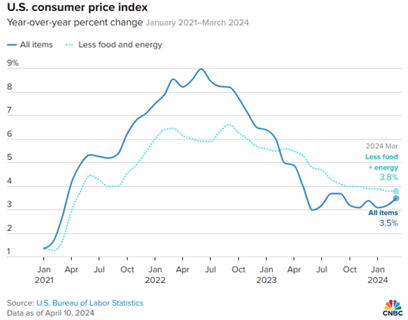

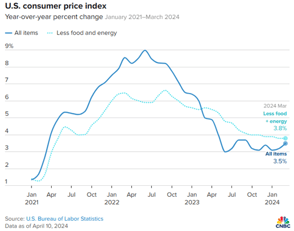

3. ‘Sticky’ Inflation

Inflation has broad-based negative impacts on the economy. We’ve all witnessed this ourselves at the grocery store or gas station. Demand was pulled forward while supply was severely limited during the pandemic (as stated above) leading to aftershocks. High inflation has caused the Fed to wait on lowering interest rates because cutting rates stimulates the economy, leading to increased demand (e.g., increase in housing transactions, business loans, etc.). The ‘dark’ side of increased demand is often higher inflation which remains the number one concern for Americans today (Gallup). Rates have stayed higher for longer due to the perception that the economy is not weakening. However, there are increasing signs of a slowing economy, which ironically may be positive for the markets as it allows the Fed to start cutting interest rates.

However, if inflation remains high (Fed Target: 2%) and the Fed continues to delay rate cuts it hampers business growth. Higher-than-expected inflation is why stocks slightly sold off in April and remains the largest known risk for US stocks in my opinion.

Bonds have also performed poorly due to multiple Fed rate hikes in 2022 and 2023 (higher rates = lower bond returns). However, bonds provide much better yields than a few years ago with high-yield savings accounts at ~5%. While these rates will likely come down if and when the Fed lowers rates, diversified bond portfolios should benefit (lower rates = higher returns) following a really tough stretch over the past few years. Bonds play an important income generation and potential principal protection role in investors’ portfolios.

Advisory services are offered through Hevel Capital, LLC., an Investment Advisor in the State of California. All content is for information purposes only. It is not intended to provide any tax or legal advice or provide the basis for any financial decisions. Nor is it intended to be a projection of current or future performance or indication of future results. Purchases are subject to suitability. This requires a review of an investor’s objective, risk tolerance, and time horizons. Investing always involves risk and possible loss of capital. This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. This information should not be relied upon by the reader as research or investment advice regarding any funds or stocks in particular, nor should it be construed as a recommendation to purchase or sell a security. Past performance is no guarantee of future results. Investments will fluctuate and when redeemed may be worth more or less than when originally invested.

Source: Jabil

3857 Pell PL Unit 103 San Diego, CA 92130

mk@hevelcapital.com

(636) 236-9039

All content is for information purposes only. It is not intended to provide any tax or legal advice or provide the basis for any financial decisions. Nor is it intended to be a projection of current or future performance or indication or future results.

Opinions expressed herein are solely those of Hevel Capital, LLC and our editorial staff. The information contained in this material has been derived from sources believed to be reliable but is not guaranteed as to accuracy and completeness and does not purport to be a complete analysis of the materials discussed. All information and ideas should be discussed in detail with your individual adviser prior to implementation. Advisory services are offered by Hevel Capital, LLC an Investment Advisor in the State of California. Being registered as an investment adviser does not imply a certain level of skill or training.

The information contained herein should in no way be construed or interpreted as a solicitation to sell or offer to sell advisory services to any residents of any State other than the State of California or where otherwise legally permitted.

Images and photographs are included for the sole purpose of visually enhancing the website. None of them are photographs of current or former Clients. They should not be construed as an endorsement or testimonial from any of the persons in the photograph.

Purchases are subject to suitability. This requires a review of an investor’s objective, risk tolerance, and time horizons. Investing always involves risk and possible loss of capital.